“Demography is destiny.” — Auguste Comte

At Mainstay Financial, much of our investment analysis begins with a simple question: where are population patterns quietly reshaping the future demand for senior housing? While capital markets often focus on current headlines or the largest metropolitan areas, long-term senior housing demand is determined by demographic shifts that unfold gradually over decades. Understanding where population cohorts are forming today can provide early insight into where senior housing demand will emerge twenty years from now.

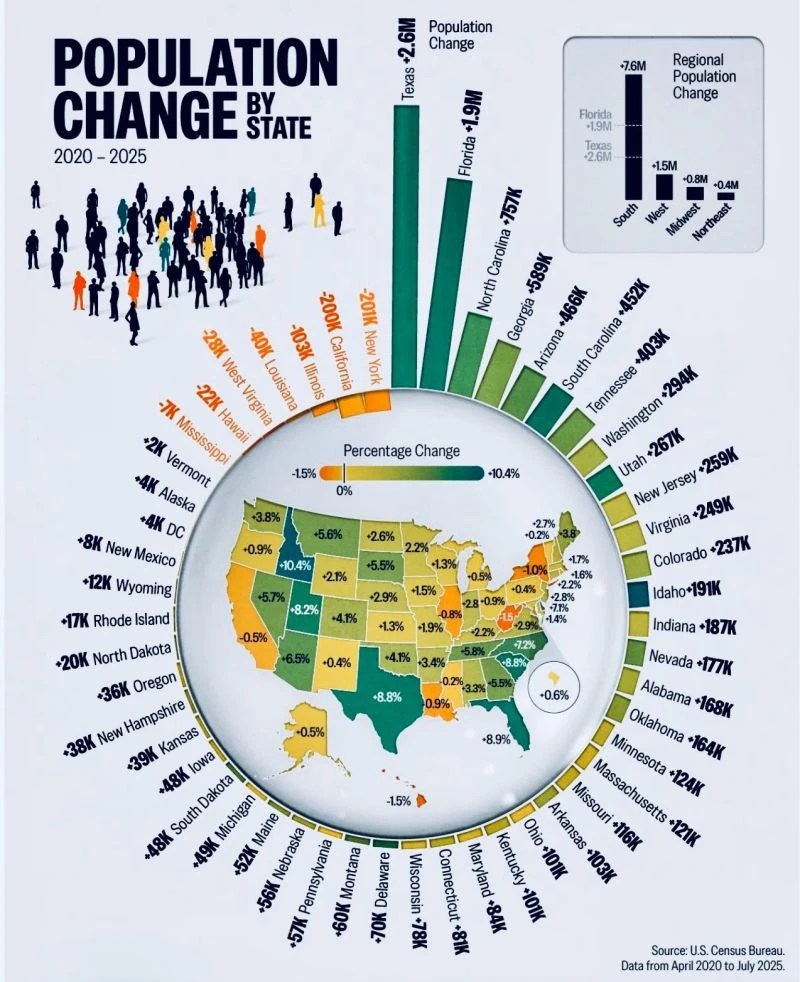

Between 2020 and 2025, the United States added more than ten million residents. On the surface, that statistic simply confirms that the country continues to grow. The deeper story, however, is not the growth itself—it is where people are choosing to live.

Over the past several years, migration patterns have quietly reshaped the economic geography of the United States. The South alone absorbed more than 7.6 million new residents during that period. Texas added roughly 2.6 million people, while Florida gained nearly 1.9 million. North Carolina and Georgia together added more than 1.3 million residents. These migration patterns carry significant implications for housing markets, healthcare infrastructure, and regional economic development across the country.

Most observers look at these numbers and draw a familiar conclusion: the Sunbelt is expanding while other regions experience slower growth. Yet when these patterns are viewed through the lens of senior housing investment, a more nuanced question emerges. Where are the population cohorts forming that will ultimately drive the next generation of senior housing demand?

For investors focused on the middle-market segment of senior housing, the answer may not lie primarily in the nation’s largest metropolitan areas. Increasingly, the data suggests that secondary and tertiary regional markets may shape the next decade of senior housing investment.

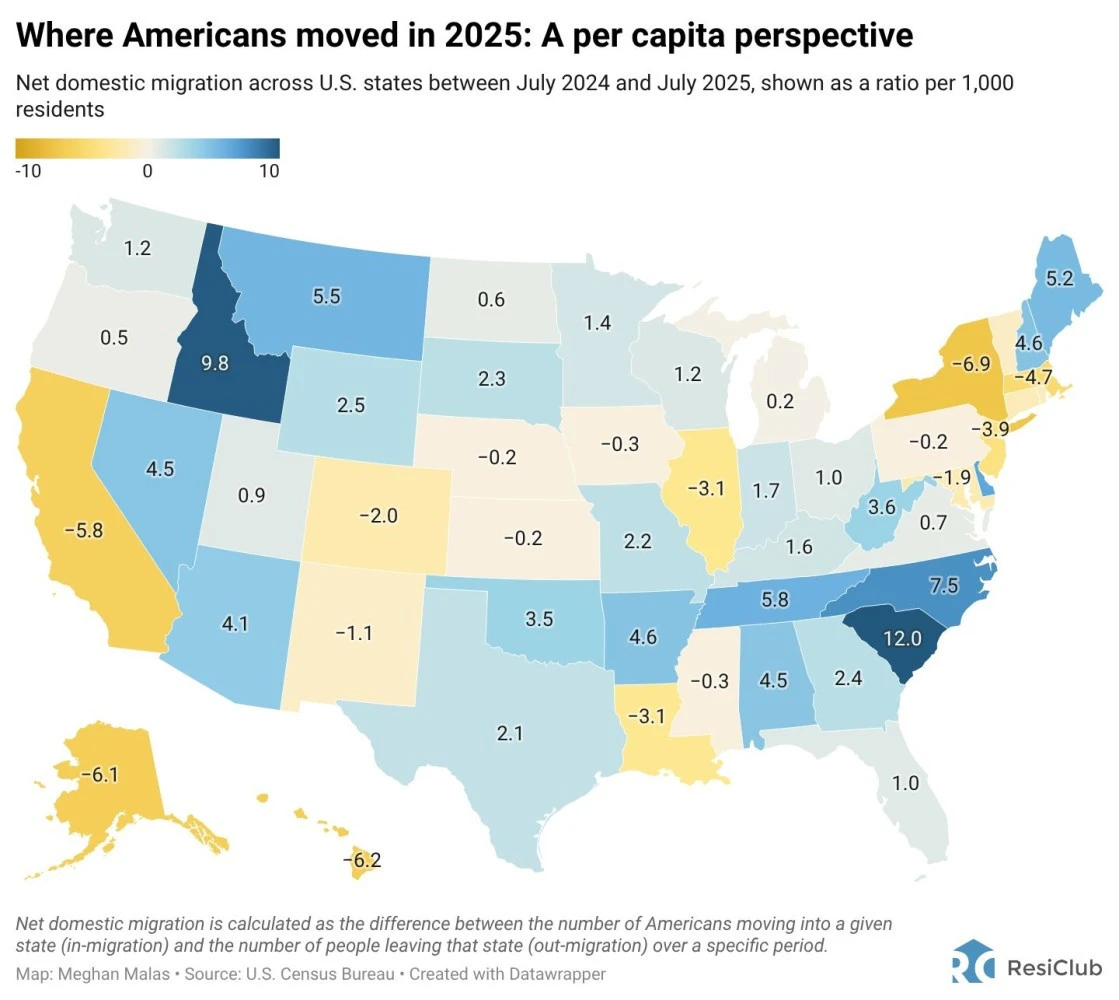

A closer look at migration data reveals an important underlying pattern. When population movement is measured on a per-capita basis, several of the fastest-growing states are not necessarily the largest Sunbelt markets. Instead, many of them are states where population growth is spreading outward into secondary and tertiary regional corridors.

States such as South Carolina, Tennessee, North Carolina, Idaho, and portions of the Mountain West have experienced some of the highest inbound migration rates in the country. Rather than concentrating exclusively in large metropolitan centers, population growth is diffusing into strong regional hubs where employment opportunities, healthcare infrastructure, and housing affordability create attractive long-term living environments.

Cities such as Greenville, Chattanooga, Huntsville, Lakeland, Knoxville, and Wilmington are examples of these regional centers. While they may not be global gateway cities, they function as important economic anchors within their regions. Healthcare systems are expanding, employment bases are diversifying, and housing costs remain comparatively accessible.

Many of the households relocating to these communities are in their late forties, fifties, or early retirement years. When individuals relocate during this stage of life, they often establish long-term roots. As a result, the senior housing demand of 2035 and 2045 is quietly forming today. Entire population cohorts are relocating to these regions and aging there together.

This dynamic creates a structural consideration for the senior housing industry.

For much of the past two decades, senior housing development followed a relatively consistent model. Projects were concentrated in large metropolitan markets and often designed with hospitality-style amenities targeted toward affluent private-pay residents. During periods of inexpensive capital and strong development cycles, this approach generated attractive returns for investors and operators.

Today the operating environment looks different. Construction costs remain elevated, labor shortages continue to challenge operators, and higher interest rates have reshaped the economics of new development. In many markets, the rents required to justify new construction now exceed what middle-income retirees can reasonably afford.

The result is a widening gap between what the industry builds and what the market actually needs. This issue is often described as the “middle-market problem” in senior housing. Yet the geographic dimension of that problem is frequently overlooked.

Secondary and tertiary markets may offer a different path forward. In many of these regions, land costs remain lower, development competition is less intense, and projects can be designed at a scale that supports disciplined capital deployment. Healthcare infrastructure continues to expand alongside population growth, and workforce stability can sometimes be stronger than in large metropolitan markets where labor competition is particularly intense.

At the same time, these regional communities are absorbing steady migration from households seeking affordability, lifestyle stability, and access to healthcare. As those residents age, demand for assisted living, memory care, and supportive housing will follow.

The opportunity is not simply to build more senior housing. The opportunity is to build the right kind of housing in the places where the aging population is actually forming.

From a capital allocation perspective, the coming decade may reward a shift in thinking. Instead of concentrating primarily on luxury developments in major metropolitan markets, senior housing portfolios may increasingly expand into regional growth corridors. These markets often require a different development mindset—one focused on disciplined construction costs, operational efficiency, and care models designed for middle-income households.

Amenities may matter less than operational reliability. Community integration may matter more than architectural spectacle. In many ways, the next generation of senior housing may resemble regional aging infrastructure more than hospitality-driven real estate development.

Demographic change rarely arrives suddenly. It unfolds gradually through migration patterns, economic opportunity, and the places people ultimately choose to call home. Today’s migration map already offers a glimpse of where the next generation of senior housing demand will emerge.

Across regional growth corridors throughout the Sunbelt and beyond, communities are quietly absorbing the population cohorts that will shape the industry’s future. For investors, operators, and developers, the question is not whether these demographic forces will matter. The real question is whether capital strategies are evolving quickly enough to recognize them.

Clarity Brief Insight

Population migration today determines senior housing demand two decades from now. The most important markets may not be today’s largest metropolitan areas, but the regional growth corridors where entire population cohorts are aging together.

---

About the Author: Tod Petty serves as Chief Investment Officer at Mainstay Financial Services & Mainstay Senior Living, where he leads capital strategy, investor alignment, and portfolio growth across an operationally informed senior housing platform. With more than three decades of experience as an owner, operator, and executive, he focuses on disciplined acquisitions, resilient middle-market communities, and capital structures designed to perform across cycles.